From a prudential and welfare perspective, the judgment on private credit is mixed. On the one hand, it fills a gap between retail bank financing to SMEs, mainly provided by banks, and wholesale public markets, reserved for large listed corporates. On the other hand, private credit becomes a problem if it practices regulatory arbitrage to elude prudential safeguards

The following is an excerpt from the written evidence that Ignazio Angeloni provided to the UK House of Lords Financial Services Regulation Committee on the topic of Private markets and financial stability.

You can read the full document here

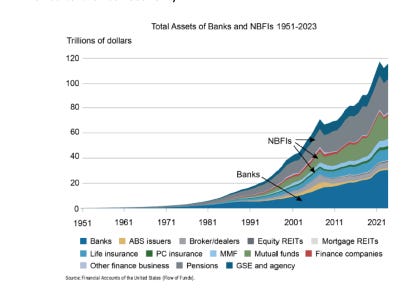

In recent decades, especially after the Great Financial Crisis of 2008-2009 (GFC), segments of financial intermediation have increasingly shifted outside the banking sector, towards the so-called non-bank financial institutions (NBFIs).

NBFIs are a heterogeneous collection of financial institutions comprising insurance companies, pension and mutual funds, broker-dealers, private equity and private credit funds, financial companies, special-purpose vehicles, etc.

This transition has been massive in the US but significant in Europe and other areas as well.

Some entities within the NBFI universe have started performing functions previously reserved to banks, direct lending being one of them, hence acquiring greater importance in providing finance to the real economy.

Several reasons are behind this phenomenon.

One has been the tighter regulation imposed on banks after the GFC, with higher capital and liquidity requirements imposed especially on large systemic banks.

Another reason is population ageing, which increases the demand for pension and insurance products, hence channelled a growing flow of funds to the NBFI sector; private credit, to which we will turn in a moment, is partly financed by insurance companies.

Finally, another driver has been the long period of ultra-low interest rates, which rendered bank intermediation less profitable and led investors to search for more attractive returns outside the banking sector.

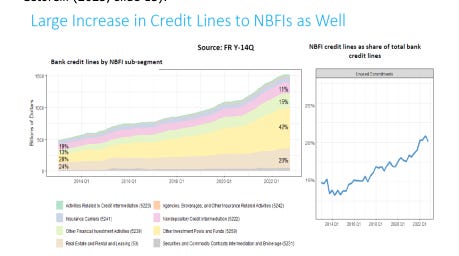

NBFIs and their interconnections with the banking sector have increased in tandem, taking many forms. Acharya et al (2024) report estimates of the interconnections among the components of the NBFI sector. Bank credit exposures to NBFIs have increase steadily, see chart below from Cetorelli (2025, slide 13).

Banks are the main providers of liquidity and short-term finance to insurance companies and other non-financial intermediaries.

Moreover, banks own large stakes in the asset management sector, implying that they suffer financially if NBFIs, which are part of their group, get into trouble even if incorporated separately.

In some cases, banks may feel a reputational responsibility towards non-bank entities they are associated with.

Conversely, NBFIs maintain their liquid balances with banks and contribute to funding them also in different ways, e.g., by holding bonds and subordinated capital instruments. NBFIs are also users bank services; for example, to transact in their behalf if they do not have direct access to central counterparties (CCPs). Therefore, interrelations run both ways.

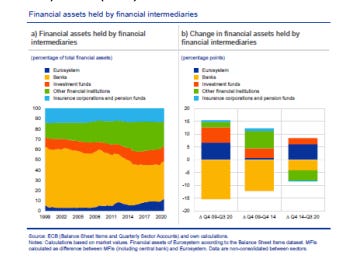

In Europe, bank exposures to NBFIs are more limited so far. Data reported by the Basel Committee on Banking Supervision (2025) show that bank funding of NBFIs in Europe has stood at just below 10% of total balance sheets in recent years, whereas funding provided by NBFIs to banks stood at around 15%.

However, it must be considered that these are average figures; bilateral exposures can be significantly higher, as they are highly concentrated in a few large GSIBs (Globally Systemic Important Banks).

Private credit

Private credit is a particular manifestation of this general phenomenon, of growing importance in recent times. It consists of a diversified class of non-bank intermediaries – insurance companies, hedge funds, pension funds, venture capital and private equity funds, Business Development Companies (BDCs), etc – providing debt finance to nonfinancial businesses. Private debts are not publicly traded and are typically bespoke: covenants and returns are agreed bilaterally on a case-by-case basis.

Borrowers are typically mid-size businesses, between 100 mn and 1 bn US$ of annual revenue, too large for being funded by banks but too small to directly access public markets. Maturity is usually long (5 years or more), beyond that of average bank exposures but matching the investment horizon of certain NBFIs, particularly insurance and pension funds.

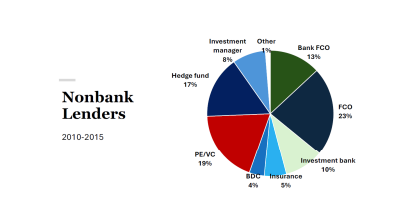

Data on the breakdown of private credit by instrument, originating institution, and ultimate investors are limited, which makes it difficult to assess the phenomenon. An estimate of the investor breakdown from Erel (2025), calculated on a sample of listed borrowers only, is shown below

As one can see, the most important categories are hedge funds, private equity (PE) funds, Venture Capital (VC) funds, and financial companies, partly affiliated with banks.

Minor shares are represented by BDCs, specialized lenders required by US law to invest 70% of their assets in mid-size companies, insurance, and investment banks.

Private credit is one of the fastest-growing asset classes in recent years. Outstanding private credit is now estimated to be over 2 trillion US$ globally (IMF, 2024), of which about two thirds in the US. This is about eight times the size before the GFC. By comparison, total bank assets in the US today are about ten times as large as private credit.

Private credit has grown larger than leveraged loans and high-yield bonds, the other two main components of risky corporate debt.

In Europe, the phenomenon is much smaller but growing; assets under management of private credit funds in 2024 stood at €0.43 trillion, against €0.15 trillion euro in 2014. By comparison, private equity grew in the same period from €0.4 trillion to €1.2 trillion.

Private credits are riskier than bank loans or large syndicated loans, in particular because they have lower recovery rates after default, though default rates are lower.

It has been shown that the probability of borrowing from a non-bank rises sharply when a company’s profitability falls below zero, indicating that private debt collects fringes of credit markets that bank regulation excludes from traditional channels.

Gross returns are higher in private credit than in most other asset classes; however, analysis by Erel et al (2024) suggests that extra returns are just sufficient to compensate for risk and fees, so that risk-adjusted net abnormal returns for investors are indistinguishable from zero.

Haque et al. (2025) find that a large share of companies borrowing from private credit lenders also borrow from banks; the two forms of finance appear to be complementary and to serve different purposes: private lenders providing long-term investment-related financing, banks acting as liquidity providers by means of credit lines.

The synergy and the division of roles between the two functions is driven by tax and regulatory distortions, as well as organizational convenience.

In the US, private credit enjoys political support from the Trump administration; a recent presidential executive order instructs the Treasury and the Securities and Exchange Commission to “… consider ways to facilitate access to investments in alternative assets by participants in participant-directed defined-contribution retirement savings plans”. “Alternative assets” is a broad categorization of illiquid and non-publicly-traded assets, including private credit.

Benefits and risks from private credit

From a prudential and welfare perspective, the judgment on private credit is mixed. On the one hand, it is a valuable addition to financial markets, filling a gap between retail bank financing to SMEs, mainly provided by banks, and wholesale public markets (equity and debt), reserved to large listed corporates.

It also helps match the preferences of mid-market companies in terms of size, cost, and maturity of debt, with those of asset managers with longer horizons such as life insurers and pension funds.

On the other hand, private credit becomes a problem if it practices regulatory arbitrage to elude prudential safeguards, if it makes use of opaque instruments whose risks are hard to assess by investors and regulators, and if its links with the traditional financial sector give rise to contagion and systemic risks.

All three dangers are present at this moment, though the extent is difficult to assess due to a lack of data.

For these reasons, private credit justifiably attracts special scrutiny and attention by regulators and supervisors.

One reason for concern is that part of private credit is financed through opaque multilayered funding structures that make it difficult to understand the risk involved.

Typically, the originating company, an insurer or other asset manager, may issue Funding Agreement-Backed Notes (FABNs) to special purpose entities, whose funding instruments are in turn subscribed by a host of leveraged investors like hedge funds, banks, high-wealth individuals, and so on.

The funding chain may include Collateralized Loan Obligations (CLOs), securitized instruments obtained by repackaging and selling tranches of private credit assets. Funding may involve BDCs, closed-end funds which, as already mentioned, are required by law to invest at least 70% of their balance sheet in private assets issued by SMEs; BDCs fund themselves by issuing shares as well as debt.

Chernenko et al (2025) showed that BDCs are more capitalized than banks with similar risk profile; this makes for a lower solvency risk than if the corresponding credit were granted by banks.

However, the funding structure of this asset class is continuously evolving, as new instruments and intermediaries are introduced. Data reporting struggles to keep up with innovation; hence, regulators lack sufficient information to assess the risks involved. Four dimensions of risk, in particular are hard to appreciate.

First, leverage risk.

Whereas leverage may be limited for the immediate provider of private credit, for example a BDC, it is normally greater if the entire funding chain is considered. Lack of detailed information prevents accurate assessment of the effective leverage involved in the process leading to private credit disbursement.

The second dimension is rollover risk.

FABN are typically long-term and cannot be redeemed in advance, but maturities concentrate in certain years. If market stress occurs in those years, especially if some final borrower defaults, funding vehicles may be unable to meet their obligations.

Third, interconnection risk. As seen earlier, the funding chain includes virtually all entities in the financial markets, banks as well as NBFIs; its rich structure contributes diversification but also interconnection, which is a source of systemic risk.

Partial evidence for the euro area suggests that transmission of risk through the interconnection matrix is limited so far, but this can change quickly.

Finally, credit risk. The ultimate borrowers are not only riskier than the average corporate, but their liabilities, not publicly traded, are valued less timely and accurately. It is also worth noting that funding instruments such as FABN are not individually rated; investors rely on company ratings based on the insurer’s ability to meet its policy obligation, which is usually less demanding.

The above challenges should be addressed through a 2-pronged strategy:

1. Collecting adequate information and making is available to regulators and field supervisors, so that they can monitor the phenomenon in an accurate and timely way;

2. Regulating the phenomenon (without discouraging it, because, as we argued, private credit performs a useful function) according to the principle “same activity, same risk, same regulation”.

© Copyright